The false and misleading case for the Measure B Sales Tax

Thursday, April 16th, 2026

By Marc Joffe

On Tuesday, a Contra Costa Superior Court judge declined to expedite a lawsuit demanding changes to proponents’ ballot arguments for Measure B, the county’s proposed five-year, 0.625% sales tax increase. That decision means voters will receive a County Voter Information Guide containing false and misleading statements about the tax increase.

This is not just a problem with Measure B. And it could get worse as advocates for taxes and bond measures make increasingly aggressive claims, irrespective of the facts, and without fear of a judicial remedy.

The case, filed March 27 on behalf of two Contra Costa voters, targets both the Primary Argument in Favor of Measure B and the Rebuttal Argument to the Primary Argument Against Measure B. The respondents are the five authors of those arguments, including a sitting County Supervisor.

The legal challenge was brought under California Elections Code section 9190, which allows voters to seek a writ of mandate during a 10-day public examination period to require that ballot arguments be amended or deleted if they are “false, misleading, or inconsistent with the requirements” of the law.

The Dubious Claims

The complaint identified over a dozen specific claims in the ballot arguments alleged to be false and/or misleading. Here are three that are especially notable.

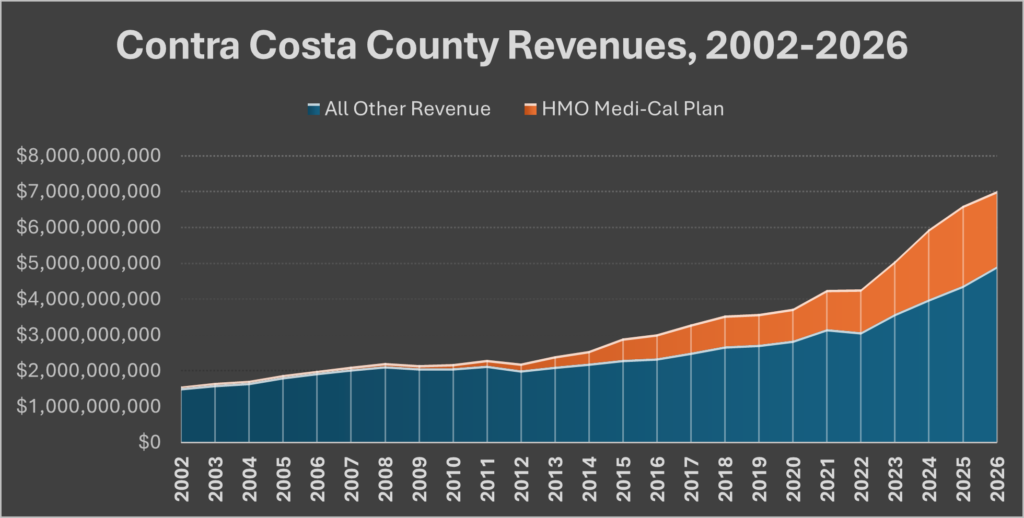

Exaggerated $1.5 Billion Loss: The argument claims that “according to the county health director, our health system will lose more than $1.5 billion over the next five years.” This appears to have been based on Board of Supervisors materials which mentioned a $300 million annual loss for the five year life of the tax.

But at the March 3 Board meeting Supervisor Candace Andersen flagged the original $300 million annual loss figure as inaccurate. The Board’s adopted Resolution No. 2026-40 was amended to project cumulative losses of approximately $239 million through 2029. The County’s own budget presentation cited a six-year cumulative figure of $509 million. This is roughly one-third the amount we will see in the voter guide.

And even the $509 million estimated loss is unlikely to materialize. With Democrats almost certain to regain control of the House (and possibly the Senate), they will be able to implement their stated intention of reversing HR1’s federal budgetary changes that impact Medi-Cal.

Further, about a quarter of the remaining estimated funding loss is attributable to scheduled reductions in federal subsidies to Disproportionate Share Hospitals (DSH) like Contra County Regional Medical Center. As we discuss on our Stop Measure B website, DSH funding cuts were first included in the 2010 Affordable Care Act and have been repeatedly postponed by Congresses controlled by both parties. It is reasonable to expect these postponements to continue through at least 2031 when the tax sunsets.

Groceries, Food, Housing, and Medical Care: The argument states “Measure B won’t increase the cost of groceries” and “It exempts food, housing, and medical care.” The petition notes that the words “food,” “groceries,” “housing,” and “medical care” appear nowhere in the Measure B ordinance’s exemptions. Hot prepared foods are subject to sales tax, as are non-food groceries. Lumber, cement, and roofing materials (items associated with housing) are taxable. Over-the-counter drugs are taxable.

90,000 People “Will” Lose Health Insurance: The argument states that “more than 90,000 people will lose health insurance” if Measure B fails (emphasis added). The word “will” makes this statement false and misleading under California election law.

Contra Costa Health staff gave supervisors a broad range of the number of beneficiaries who may lose Medi-Cal coverage due to new rules, with 90,000 being near the midpoint. These projections are estimates, contingent on future legislative and administrative decisions that have not yet been finalized. No one can say with certainty how many residents will lose coverage.

There is a further problem that the ballot argument glosses over. Even if Medi-Cal rolls shrink in Contra Costa County, it does not necessarily mean our neighbors are becoming uninsured and will flood emergency rooms. People cycle off Medi-Cal for many reasons: they move away, they obtain employer coverage, they age into Medicare, or they pass away. Proponents misleadingly conflate any reduction in Medi-Cal enrollment with people left without coverage.

Implications Beyond Measure B

Unless you read this article or the plaintiff’s court filings, you will not be aware of these inaccuracies. And that points to a serious defect in California election law.

Ballot proponents (or opponents) can make false and misleading arguments, and get away with it, because the court process usually cannot unfold quickly enough to meet the County’s aggressive timetable for editing, translating, printing, and mailing ballot guides.

To remedy this problem, process reforms are needed. Either several additional days should be added to the pre-election timetable for claims like the ones against Measure B to be heard and adjudicated. Alternatively, California should move away from printed voter guides and instead post them on the web. Not only would that provide more time to edit inaccurate arguments prior to public exposure, but taxpayers would also save money on printing and mailing costs. It would be good for the environment too!

Marc Joffe is the President of the Contra Costa Taxpayers Association.