Antioch Council to discuss ’26-’27 budget facing double digit deficit, AI assistant for police dispatch

Monday, March 23rd, 2026

Will also deal with legal matters including the ongoing civil rights class action lawsuit, potential lawsuit with “significant exposure” and two cases; Measure W spending & Economic Development reports

By Allen D. Payton

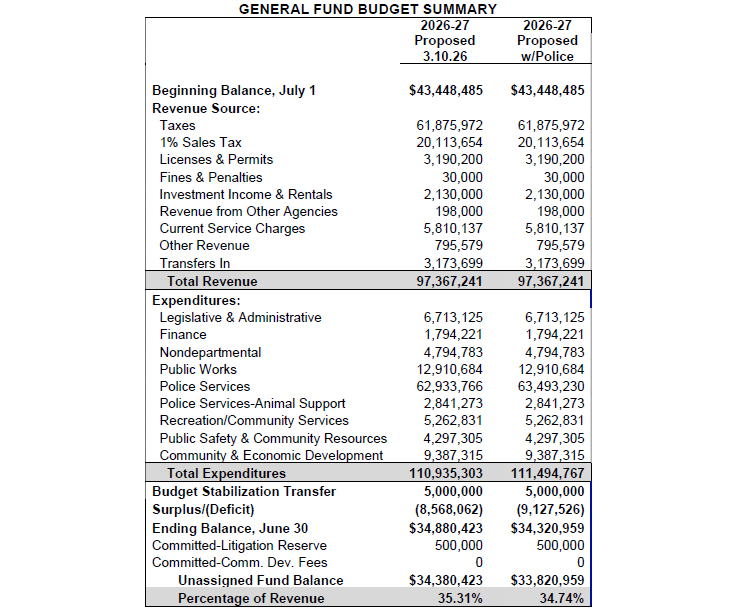

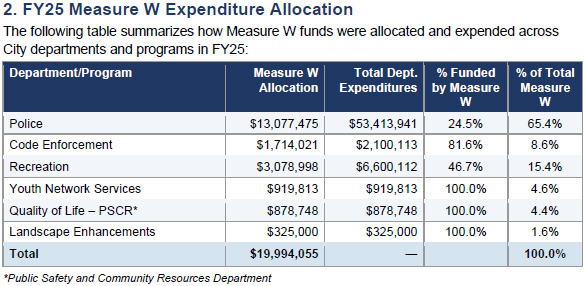

During a Special Meeting before their regular meeting on Tuesday, March 24, 2026, the Antioch City Council will discuss development of the 2026-27 Fiscal Year budget with a potential $13.5 to $14.1 million deficit. During their regular meeting the council members will also discuss approving an AI assistant for police dispatch, and receive reports on both Measure W spending, which has decreased the amount for police down to 65.4%, and economic development.

Closed Session, Lawsuits & Property Negotiations

But first, at 4:00 p.m., the Council will hold a Closed Session during which they will discuss the ongoing Trent Allen, et al. v. City of Antioch, et al., civil rights class action lawsuit that’s not yet completely settled. (See related articles here and here) They will also discuss a potential lawsuit described as, Significant Exposure to Litigation. The description for that agenda item reads, “The City is in receipt of information concerning facts and circumstances that might result in litigation against the City which are known to a potential plaintiff and that pertain to potential claims by the potential plaintiff against the City. Two cases.”

Finally, the Closed Session agenda item 3, the Council will enter into Real Property Negotiations with Lone Tree Golf & Event Center Manager Ron Parish for two properties, 4800 Golf Course Road and West 1st Street. The City owns both the Lynn House and the old Mayor Hard House on that street. UPDATE: Mayor Pro Tem Don Freitas and City PIO Jaden Baird later explained that including West 1st Street was a mistake and the negotiations are only about the golf and event center.

Budget Study Session

At 5:00 p.m., the Council will hold Special Meeting/Study Session on the 2026-27 Fiscal Year Budget Development. The City is facing a double-digit deficit of $13.5 million to $14.1 million depending if the council approves increasing the number of sworn police officers to 117.

AI Assistant for Police Dispatch

During their regular meeting, under the Consent Calendar Item J., the council will consider approving a Sole Source Agreement with Prepared to provide an AI assistive call taking system for the Police Department Dispatch Center for a two-year term, in an amount not to exceed $248,400 for Years 1 through 2, with an option to extend for three additional years.

According to the city staff report, “The Dispatch Center is currently operating with four Dispatcher vacancies out of 17 allocated positions (13 Dispatchers and 4 Leads), representing an approximately 24% vacancy rate. Call demand remains consistently high. The Police Dispatch Center handled approximately 72,000 9-1-1 calls in both 2024 and 2025. Non-emergency call activity remained steady as well, at approximately 208,000 calls annually. In addition to phone call volume, the Police Department handled 86,185 calls for service incidents in 2025, including AQCRT (Community Response Team) calls, which require ongoing dispatch coordination beyond the initial intake.”

Assistive call taking technology is intended to support Dispatchers, not replace them with the following:

- Improve Service for Non-Emergency Callers and Reduce Hold Times

- Support Emergency Calls Through “Co-Pilot” Functionality

- Improve Documentation and Reduce Staff Time Spent on Records Requests

- Expand Language Access and Support DOJ (Department of Justice) MOA (Memorandum of Understanding) Obligations

Measure W Sales Tax Citizens’ Oversight Committee Annual Report

Under Consent Calendar agenda Item N. the Council will receive the Sales Tax Citizens’ Oversight Committee Fiscal Year 2024-25 Annual Report on Measure W (1% Sales Tax). It will show the amount being spent on police has decreased from 80%, as originally intended, to now, just 65.4%.

Economic Development Update

In addition, according to the City staff report for agenda item 7, the Council receive an update on the City’s Economic Development activities and progress, provide policy direction as appropriate, and offer feedback to staff on priorities and the timing of subsequent updates to the City Council. The matter is part of the Council’s 6-Month Priority list.

Meeting Details

The regular meeting will begin at 7:00 p.m. The latter two meetings will be held in the Council Chambers at 200 H Street, or can be viewed via livestream on the City’s website or on Comcast cable TV channel 24 or AT&T U-verse channel 99.

See the complete meeting agenda packet.