Antioch Council spends $2.3 million in extra tax revenues but nothing for homeless or more cops

Wednesday, November 24th, 2021

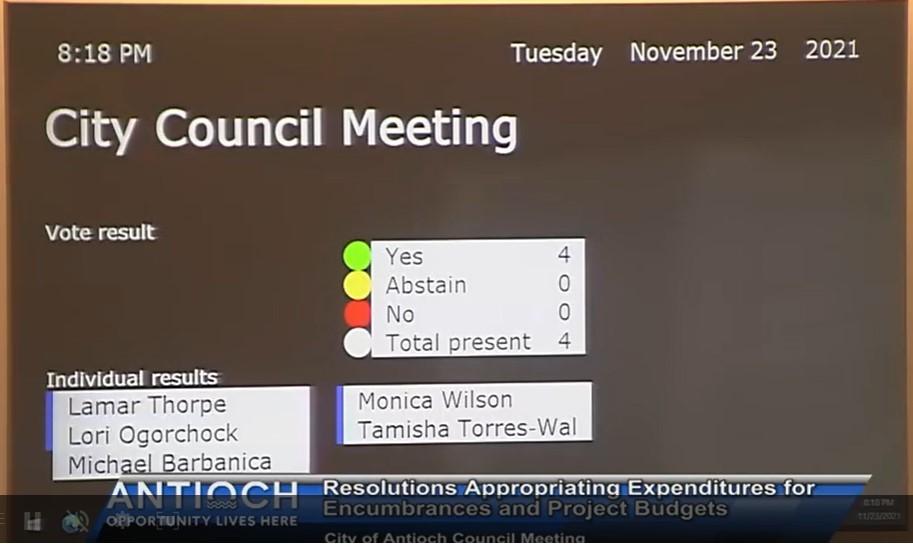

The Antioch City Council uses their new display board showing how they voted during their meeting on Tuesday, Nov. 23, 2021. Video screenshot.

Approve $1,500,000 for renovation of City Hall second floor

Thorpe, Torres-Walker want to renovate Hard House for council member offices, plus staff for each council member

By Allen Payton

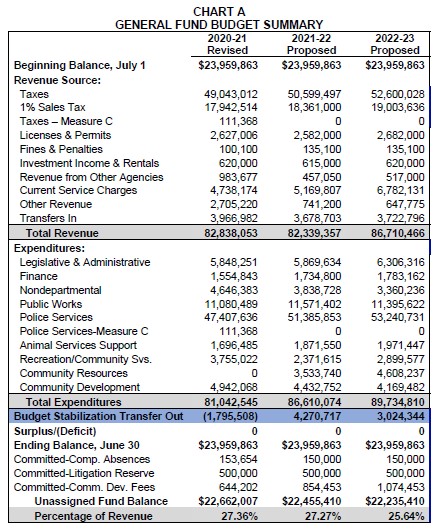

During Tuesday night’s meeting, Nov. 23, 2021, Antioch Finance Director Dawn Merchant said the city council will have an additional $2.3 million to spend in this year’s budget, with over $2.5 million additional from sales tax, including over $1.5 million more from Measure W’s 1% sales tax revenues. The council members chose to allocate the funds but included nothing to pay for more police officer or to help the homeless.

According to the City staff report on the item, “The major contributing factors to net revenues higher than projected are:

- $1,542,781 higher Measure W/1% sales tax than projected.

- $1,006,854 higher sales tax than projected.

- $435,820 more in building permit revenue than anticipated.

- $231,737 more in property tax revenue than anticipated.

- $160,000 more in interest and rental revenue than anticipated.

- Approximately $532,000 additional revenues than anticipated from various miscellaneous sources.

There was also a $1,571,461 reduction in revenues for the amount billed to the Department of Water Resources (DWR) for our usable river water days as the money was not received until October 2021 requiring us to record this revenue in FY22 instead.”

Plus, there were $6,425,217 less in expenditures than projected for Fiscal Year 2021. The major contributing factors to net expenditures lower than projected are:

$383,762 less in operating subsidy than projected to the Animal Shelter.

$557,686 less in operating subsidy than projected to Recreation programs.

$2,007,481 in salary savings from all unfilled positions. $1,051,661 represents non- Police salary savings which the City Council will need to allocate to one-time projects and/or unfunded liabilities per the City’s one-time revenue policy. The appropriation has been included in the budget amendments in Exhibit C to Attachment A.

$271,532 in purchase orders as of June 30,2021 not yet entirely spent. The carry forward of the budgets for these is included in the budget amendments in Exhibit A to Attachment A.

$1,941,089 in project budgets outstanding as of June 30, 2021, not yet entirely spent. The carryforward of the budgets for these is included in the budget amendments in Exhibit B to Attachment A.

$1,054,466 in non-salary savings in the Police Department budget.

$328,786 in non-salary savings in Public Works.

$2.85 and $3.1 Million More in FY22 and FY23

As a result, city staff is projecting increases to Fiscal Year 2022 General Fund sales tax and 1% sales tax projections by $2,849,683 and FY23 by $3,121,657 based on FY21 closing numbers and current sales tax projection trends.

Council Allocates Funds But, None for More Police Officers or Homeless

Staff also proposed how to spend the additional funds, including paying for projects the City has already begun and moving up items from the FY22 budget.

Mayor Lamar Thorpe suggested holding off on approving costs related to establishing the new Community Resources Department.

Then without any comments from the public, District 3 Councilwoman Lori Ogorchock made, and District 2 Councilman Mike Barbanica seconded a motion to approve the remaining items. But both Mayor Pro Tem Monica Wilson and Thorpe said they would rather discuss them on a item by item basis. The motion failed 2-3 with District 1 Councilwoman Tamisha Torres-Walker joining Thorpe and Wilson in voting no.

The council members then reviewed the other proposed budget items, with Thorpe seeking consensus

- Consideration of vehicles and equipment for the seven (7) new Code Enforcement Officers approved in the budget at a General Fund FY22 cost of $245,000 and $21,000 in FY23.

- Consideration of an Administrative Assistant for Human Resources. The FY22 General Fund budget cost would be $30,769 (includes $5,000 for computer and other startup costs) and $110,479 in FY23.

- Consideration of a Finance Analyst for Finance. Finance would request this not be budgeted until FY23 with a General Fund cost of $181,981, which includes $5,000 for computer and other startup costs.

- Consideration of a Community Development Technician for Community Development at a FY22 General Fund budget cost of $42,513 (includes $2,000 startup costs) and $167,253 in FY23.

- Consideration of a GIS Technician position for Public Works at a FY22 General Fund budget cost would be $32,039 and $137,554 in FY23.

- Consideration of an Administrative Assistant position for Public Works at a FY22 cost of $24,290 and $104,068 in FY23.

Items Without Consensus or to Be Brought Back Later

- Community Resources Department for an Administrative Analyst at a cost of $40,426 in FY22 and $166,894 in FY23; an Administrative Assistant at a cost of $24,290 in FY22 and $104,068 in FY23; building furnishings/remodel and repairs at an estimated cost of $1,000,000 to accommodate the staffing of the new department.

- Consideration of Prewett Park Perimeter Fence Replacement at a FY23 General Fund budget cost of $200,000.

- L Street Improvements project at a FY22 unknown funding source cost of $9,281,000.

- The plan is to wait for possible funds from the recently approved federal infrastructure bill.

- Wilson wanted a study session to discuss the various “corridors”.

- Thorpe responded, “there will be a study session.”

- Dedicated CORE Team at a General Fund cost of $250,000 in FY22 and FY23. – Both Ogorchock and Barbanica supported it, now.

- Consideration of Police Department Community Room Technology Upgrades at a FY22 General Fund cost of $300,000. – Barbanica argued that the room serves as the Emergency Operations Center.

Approve New Budget Requests

According to the city staff offered a list of new budget requests all of which the council supported. They are:

- A Recreation Coordinator for Youth Services was approved in the adopted 2021-23 budget for funding approved in FY23. This is being requested to begin funding in FY22 to assist the Youth Network Services Manager getting programs and services running. This request would add $47,726 to the FY22 General Fund budget assuming funding for 5 months.

- Promotion of a Senior Computer Technician position to a Network Administrator. The FY22 and 23 budget impacts are $2,741 and $8,724 respectively funded from the Information Services Internal Service Fund.

- Addition of one (1) Administrative Analyst I position in the City Clerk’s office to meet the work demands of running the office. The FY22 General Fund budget impact, assuming the position is filled for 3 months is $40,426 and the annual FY23 impact would be $166,894.

- Reclassification of one (1) Administrative Assistant I position in the City Clerk’s office to an Administrative Analyst I position. The FY22 and FY23 General Fund budget impact would be $6,181 and $27,060 respectively.

- Addition of two (2) General Laborer positions to be funded with NPDES funds at a FY22 cost of $47,692 and $211,960 in FY23. If these positions are approved, the NPDES reserves will be depleted beginning in FY24 and the positions will need to be funded with the General Fund starting in FY24. Public works has been installing trash capture devices in the City’s storm drain system to comply with State requirements to keep trash and pollutants from entering our streams and waterways. These trash capture devices require monthly inspections and cleaning. Public Works does not have adequate staffing to perform this work on an ongoing and continuing basis so a request for bids was issued. Bids were received and the cost of contracting this service exceeded the cost of performing this work in house with these two (2) additional positions being requested.

- Add $150,000 to the Information Systems Fund FY22 budget to cover cybersecurity measures to be put in place to protect the City’s network.

- Addition of one (1) Payroll Specialist position at a FY22 General Fund cost of and $40,527 and $168,132 in FY23. Payroll processing is a critical function of the City and is processed bi-weekly for over 350 full time employees and up to a couple hundred more part time employees depending on the season. The City currently has one full time Payroll Specialist with some additional support from an Accounting Technician and the Deputy Finance Director to process payroll. Another position is severely needed to not only handle the volume, especially with all the additional positions added in this new budget cycle, but to be able to continue processing payroll when the one position is absent.

- Reclassification of two (2) Office Assistant positions in Recreation to Administrative Assistant II positions at an estimated cost of $10,030 in FY22 and $20,254 in FY23 to the General Fund.

- Reclassification of one (1) Administrative Assistant III position in Recreation to an Administrative Analyst I position at an estimated cost of $3,849 in FY22 and $13,730 to the General Fund.

- Remodel of 2nd floor and basement of City Hall at an estimated cost to the General Fund of $1,500,000 in FY22.

City to Receive $10.8 Million More in Federal COVID Relief Funds

The City of Antioch will be receiving a total of $21,550,900 in funds from the American Rescue Plan Act (“ARPA”). $10,775,450 was received in May 2021, with the remaining balance of $10,775,450 to be received in May 2022.

A discussion item was brought to City Council on July 27th whereby City Council Members discussed holding town hall meetings within each of their respective districts to speak with community members regarding the use of funds. As a reminder, the main priorities and principals of the funding are to provide relief to:

- Support urgent COVID-19 response efforts to continue to decrease the spread of the virus and bring the pandemic under control;

- Replace public sector revenue to strengthen support for vital public services and help retain jobs;

- Support immediate economic stabilization for households and business; and

- Address systemic public health and economic challenges that have contributed to the unequal impact of the pandemic on certain populations.

- Recipients may use these funds specifically to:

- Support public health expenditures (as outlined in the interim final rule);

- Address negative economic impacts caused by the public health emergency, including economic harms to workers, households, small businesses, impacted industries and the public sector for those within a Qualified Census Tract or to other populations, households or geographic areas disproportionately impacted by the pandemic;

- Replace lost public sector revenue to provide government services to the extent of lost revenue (for the first measurement period ending calendar year December 2020, the City of Antioch has no revenue loss and therefore government services cannot be funded in this category); and

- Invest in water, sewer, and broadband infrastructure (as outlined in the interim final rule).

The Department of the Treasury has not yet issued final rules for spending of the funds which may provide further clarification and guidance from the interim final rule initially released. It is recommended that the City Council set a date for a future study session on allocation of the funds.

$1 Million in One-Time Funds, Mayor Wants to Use Them on Hard House for Council Member Offices

The Hard House on W. 1st Street in Antioch. Herald file photo from 2011.

Thorpe wanted the city to put money into the Hard House “as an extension of city hall…with offices for council members.” The brick building was the home of the City’s first mayor and is located on W. First Street next to the Lynn House Gallery and across from the Amtrak Station.

The Hard House was once proposed to be donated to a non-profit organization that planned to reinforce it to earthquake standards and completely restore the building. Other ideas were to turn it into a bistro or offices.

“It was pretty disappointing to show up here and see there was no space for city council members which is pretty telling of our role, here,” Torres-Walker said. She also asked to have staff for individual council members to come back for a future discussion.

“I agree with Councilwoman Torres-Walker regarding staffing support,” Thorpe said. “The public believes we are full-time, but we have full-time jobs. I believe it’s long past due.”

Ogorchock wanted all the funds to be spent to pay down the City’s unfunded liabilities.

But upon advice from City Manager Ron Bernal who said the staff could come back with more details on the proposals, it was decided the council will hold off on deciding how to spend the one-time funds.

During

During